The content below is a Jupyter Notebook converted to markdown following the instructions of this blog. This allows for publishing of Jupyter Notebook’s using blogdown. Everything appears to work except for the rendering of tables. That will be something to resolve. Table formatting notwithstanding, it doesn’t really look as nice as the standard Jupyter Notebook format. I’ve therefore linked the original here.

Introduction

This notebook will implement a rolling out of sample forecast on time series data. The aim of this notebook is to set up the initial infrastructure while allowing for subsequent iteration. Getting the piping to work, so to speak. Subsequent iterations will add an inner loop allowing for nested cross validation. This will be used to tune hyper-parameters in a time series context.

We will forecast the S&P500 index using an Elastic net logistic regression. This will be implemented using Scikit Learn’s SGDClassifier specifying the loss function “log” and penalty “elasticnet”. This specification will result in a regularised logistic regression whereby parameter may be excluded from the model via the shrinkage operator.

A key output of the notebook is a time series of the co-efficients of the parameters included in model. This will allow for assessment of the stability of the model over time.

# Import required libraries

import numpy as np

import pandas as pd

from pandas.plotting import register_matplotlib_converters

register_matplotlib_converters()

import datetime

import math

import seaborn as sns

import matplotlib as mpl

import matplotlib.pyplot as plt

import matplotlib.dates as mdates

plt.rcParams["figure.figsize"] = (12, 8)

import sklearn.metrics as metrics

from sklearn import linear_model

from sklearn.metrics import confusion_matrix

from sklearn.preprocessing import StandardScaler

The data. It comes from this R script. The data contains an attribute y1, which is a binary indicator that looks forward over the next 6 months and returns 1 if the maximum drawdown is more than 20% or the return is less than 2.5%.

Below we convert dates stored as string to the datetime format and then set this date as the index.

# Read csv fle from github

url = 'https://raw.githubusercontent.com/Brent-Morrison/Misc_scripts/master/econ_fin_data.csv'

df_raw = pd.read_csv(url)

# Convert date to datetime and create month end date

df_raw['date'] = pd.to_datetime(df_raw['date'], format='%Y-%m-%d')

df_raw['me_date'] = pd.Index(df_raw['date']).to_period('M').to_timestamp('M')

# Set date as index in new df

df = df_raw.set_index('me_date')

# Inspect csv data - shape

df.shape

(899, 47)

Some simple feature engineering for attributes that may forecast stock returns. We are not too concerned about the data and model form at this stage. Remember we are just getting the piping to work.

# Creation of attributes

df = df.assign(

CRED_SPRD = df.BAA - df.AAA

,YLD_SPRD = df.GS10 - df.FEDFUNDS

,LOAN_GROWTH = np.log(df.LOANS / df.LOANS.shift(6))

)

# Inspect csv data - first and last records

df.iloc[np.r_[0:4, len(df) - 4:len(df)],]

| date | AAA | ACDGNO | AHETPI | AWHMAN | BAA | BOGMBASE | CFNAIDIFF | CPIAUCSL | CPILFESL | FEDFUNDS | GS10 | GS2 | INDPRO | ISRATIO | KCFSI | LOANS | M2SL | NEWORDER | PERMIT | TB3MS | TWEXMMTH | UNRATE | IC4WSA | NEWORD | HMI | P | D | E | CPI | Fraction | Rate.GS10 | Price | Dividend | Earnings | CAPE | low | close | volume | rtn_m | fwd_rtn_m | rtn_6m | min_6m | dd_6m | flag | y1 | diff_flag | CRED_SPRD | YLD_SPRD | LOAN_GROWTH | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| me_date | ||||||||||||||||||||||||||||||||||||||||||||||||||

| 1945-01-31 | 1945-01-01 | 2.69 | NaN | NaN | 45.5 | 3.46 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 16.8372 | NaN | NaN | NaN | NaN | NaN | NaN | 0.38 | NaN | NaN | NaN | NaN | NaN | 13.490000 | 0.643333 | 0.940000 | 17.8000 | 1945.041667 | 2.370 | 189.448293 | 9.034717 | 13.200993 | 11.960463 | 13.210000 | 13.470000 | 0 | 0.000000 | 0.059795 | NaN | NaN | NaN | NaN | 0.0 | NaN | 0.77 | NaN | NaN |

| 1945-02-28 | 1945-02-01 | 2.65 | NaN | NaN | 45.5 | 3.41 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 16.7818 | NaN | NaN | NaN | NaN | NaN | NaN | 0.38 | NaN | NaN | NaN | NaN | NaN | 13.940000 | 0.646667 | 0.950000 | 17.8000 | 1945.125000 | 2.355 | 195.767917 | 9.081539 | 13.341429 | 12.341754 | 13.500000 | 14.300000 | 0 | 0.059795 | -0.049455 | NaN | NaN | NaN | NaN | 0.0 | 0.0 | 0.76 | NaN | NaN |

| 1945-03-31 | 1945-03-01 | 2.62 | NaN | NaN | 45.3 | 3.38 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 16.6710 | NaN | NaN | NaN | NaN | NaN | NaN | 0.38 | NaN | NaN | NaN | NaN | NaN | 13.930000 | 0.650000 | 0.960000 | 17.8000 | 1945.208333 | 2.340 | 195.627481 | 9.128346 | 13.481865 | 12.323310 | 13.390000 | 13.610000 | 0 | -0.049455 | 0.086521 | NaN | NaN | NaN | NaN | 0.0 | 0.0 | 0.76 | NaN | NaN |

| 1945-04-30 | 1945-04-01 | 2.61 | NaN | NaN | 45.0 | 3.36 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | 16.3664 | NaN | NaN | NaN | NaN | NaN | NaN | 0.38 | NaN | NaN | NaN | NaN | NaN | 14.280000 | 0.650000 | 0.973333 | 17.8000 | 1945.291667 | 2.325 | 200.542744 | 9.128346 | 13.669109 | 12.631867 | 13.670000 | 14.840000 | 0 | 0.086521 | 0.011390 | NaN | NaN | NaN | NaN | 0.0 | 0.0 | 0.75 | NaN | NaN |

| 2019-08-31 | 2019-08-01 | 2.98 | 44576.0 | 23.60 | 41.5 | 3.87 | 3271378.0 | -0.09 | 256.300 | 264.245 | 2.13 | 1.63 | 1.57 | 109.9273 | 1.4 | -0.33 | 9883.1084 | 14930.9 | 68901.0 | 1425.0 | 1.95 | 92.2746 | 3.7 | 216750.0 | 47.2 | 67.0 | 2897.498182 | 56.839092 | 134.063333 | 256.5580 | 2019.625000 | 1.630 | 2909.712357 | 57.078692 | 134.628467 | 28.704955 | 2822.120117 | 2926.459961 | 79599440000 | -0.018257 | 0.017035 | 0.049729 | 2722.270020 | -0.022599 | 0.0 | NaN | NaN | 0.89 | -0.50 | 0.022257 |

| 2019-09-30 | 2019-09-01 | 3.03 | 43233.0 | 23.67 | 41.5 | 3.91 | 3202682.0 | -0.24 | 256.358 | 264.595 | 2.04 | 1.70 | 1.65 | 109.5940 | 1.4 | -0.35 | 9902.6579 | 15028.3 | 68533.0 | 1391.0 | 1.89 | 92.6991 | 3.5 | 212750.0 | 47.3 | 68.0 | 2982.156000 | 57.220000 | 133.460000 | 256.7590 | 2019.708333 | 1.700 | 2992.382665 | 57.416224 | 133.917673 | 29.228182 | 2891.850098 | 2976.739990 | 73992330000 | 0.017035 | 0.020226 | 0.048998 | 2728.810059 | -0.037965 | 0.0 | NaN | NaN | 0.88 | -0.34 | 0.019858 |

| 2019-10-31 | 2019-10-01 | 3.01 | 42476.0 | 23.76 | 41.4 | 3.92 | 3252830.0 | -0.22 | 257.271 | 265.011 | 1.83 | 1.71 | 1.55 | 108.6714 | 1.4 | -0.51 | 9931.7438 | 15195.0 | 69267.0 | 1461.0 | 1.65 | 92.3729 | 3.6 | 215000.0 | 49.1 | 71.0 | 2977.680000 | NaN | NaN | 257.3460 | 2019.791667 | 1.710 | 2981.076008 | NaN | NaN | 28.838509 | 2855.939941 | 3037.560059 | 77564550000 | 0.020226 | 0.033480 | 0.030664 | 2728.810059 | -0.076525 | 0.0 | NaN | NaN | 0.91 | -0.12 | 0.020239 |

| 2019-11-30 | 2019-11-01 | 3.06 | 42476.0 | 23.83 | 41.4 | 3.94 | 3315603.0 | -0.22 | NaN | NaN | 1.55 | 1.81 | 1.61 | NaN | 1.4 | NaN | NaN | NaN | NaN | NaN | 1.54 | 92.4113 | 3.5 | 217750.0 | 47.2 | 70.0 | 3120.460000 | NaN | NaN | 257.6395 | 2019.875000 | 1.820 | 3120.460000 | NaN | NaN | 30.008420 | 3050.719971 | 3140.979980 | 72179920000 | 0.033480 | 0.001568 | 0.132185 | 2728.810059 | -0.008484 | 0.0 | NaN | NaN | 0.88 | 0.26 | NaN |

To the modelling. Select the attributes to be predictors and label in our model.

# List variables

# Dependent variable

dep_var = ['y1']

# Predictors/ independent variables

ind_vars = ['CRED_SPRD', 'YLD_SPRD', 'LOAN_GROWTH', 'rtn_6m']

# Other variables to be used in the plot

oth_vars = ['close']

vars = dep_var + ind_vars + oth_vars

df = df[vars]

Our new data frame.

# Drop na' when variables are not null / Nan

df = df.dropna(subset = vars)

# Inspect csv data - first and last records

df.iloc[np.r_[0:4, len(df) - 4:len(df)],]

| y1 | CRED_SPRD | YLD_SPRD | LOAN_GROWTH | rtn_6m | close | |

|---|---|---|---|---|---|---|

| me_date | ||||||

| 1954-07-31 | 0.0 | 0.61 | 1.50 | 0.006512 | 0.168940 | 30.879999 |

| 1954-08-31 | 0.0 | 0.62 | 1.14 | 0.016628 | 0.131665 | 29.830000 |

| 1954-09-30 | 0.0 | 0.58 | 1.32 | 0.019759 | 0.181765 | 32.310001 |

| 1954-10-31 | 0.0 | 0.59 | 1.58 | 0.026823 | 0.114238 | 31.680000 |

| 2019-03-31 | 0.0 | 1.07 | 0.16 | 0.029602 | -0.027690 | 2834.399902 |

| 2019-04-30 | 0.0 | 1.01 | 0.11 | 0.028409 | 0.082800 | 2945.830078 |

| 2019-05-31 | 0.0 | 0.96 | 0.01 | 0.028386 | -0.002943 | 2752.060059 |

| 2019-06-30 | 0.0 | 1.04 | -0.31 | 0.025044 | 0.159981 | 2941.760010 |

Lets get modelling. The variables defined in the next cell inform the training and testing ranges.

# Set training and testing ranges

train_length = 300

test_length = 4

loops = math.floor((len(df) - train_length) / test_length)

start = len(df) - (loops * test_length + train_length)

stop = math.floor((len(df) - train_length) / test_length) * test_length

# Empty objects

y_pred_prob = None

model_coef = None

The training, testing loop. This piece of code selects a training subset, fits a model and then applies that model to new unseen data. Predicted probabilities, and parameter co-efficients are returned to a dataframe.

# Training loop

for i in range(start, stop, test_length):

# Model data

y_train_raw = np.array(df.iloc[i:i + train_length, 0])

x_train_raw = np.array(df.iloc[i:i + train_length, 1:len(vars) - 1])

y_test_raw = np.array(df.iloc[i + train_length:i + train_length + test_length, 0])

x_test_raw = np.array(df.iloc[i + train_length:i + train_length + test_length, 1:len(vars) - 1])

# Scale for model ingestion

sc = StandardScaler()

x_train = sc.fit_transform(x_train_raw)

# Apply mean and standard deviation from transform applied to training data to test data

x_test = sc.transform(x_test_raw)

# Specify model

sgd = linear_model.SGDClassifier(

loss = 'log'

,penalty = 'elasticnet'

,max_iter = 2500

,n_iter_no_change = 500

,tol = 1e-3)

# Train model

sgd.fit(x_train, y_train_raw)

# Predict on test data and write to array

y_pred = sgd.predict_proba(x_test)

if y_pred_prob is None:

y_pred_prob = y_pred

else:

y_pred_prob = np.concatenate((y_pred_prob, y_pred))

# Capture co-efficients and write to array

coef = np.repeat(

np.append(

sgd.intercept_[0],

sgd.coef_).reshape((1, -1)),

test_length,

axis = 0

)

if model_coef is None:

model_coef = coef

else:

model_coef = np.concatenate((model_coef, coef))

# Create predictions dataframe with date index

df_preds = pd.DataFrame(

data = y_pred_prob

,index = pd.date_range(

start = df.index[train_length + start]

,periods = stop

,freq = 'M')

,columns = [0, 1]

)

# Theshold for hard prediction, to populate confusion matrix

df_preds = df_preds.assign(pred = np.where(df_preds[1] > 0.25, 1, 0))

# Join predictions to df & rename prediction to pred_prob

df_preds = df_preds.join(df, how = 'inner')

df_preds = df_preds.rename(columns = {1:'pred_prob'}).drop(columns = 0)

df_preds.y1 = df_preds.y1.astype(int)

df_preds.close = np.log(df_preds['close'])

# Create co-efficients dataframe with date index

ind_vars.insert(0, 'Int')

ind_vars = [x + '_coef' for x in ind_vars]

df_model_coef = pd.DataFrame(

data = model_coef

,index = pd.date_range(

start = df.index[train_length + start]

,periods = stop

,freq = 'M')

,columns = ind_vars

)

# Join predictions & co-efficients df's

df_preds_coefs = df_preds.join(df_model_coef, how = 'inner')

Lets inspect the dataframe containing the prediction probability, predictors, intercept and co-efficients.

# Inspect dataframe of prediction probability

df_preds_coefs.iloc[np.r_[0:4, len(df_preds_coefs) - 4:len(df_preds_coefs)],]

| pred_prob | pred | y1 | CRED_SPRD | YLD_SPRD | LOAN_GROWTH | rtn_6m | close | Int_coef | CRED_SPRD_coef | YLD_SPRD_coef | LOAN_GROWTH_coef | rtn_6m_coef | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1979-07-31 | 0.564997 | 1 | 0 | 1.09 | -1.52 | 0.084374 | 0.038092 | 4.642562 | -0.850876 | -0.059612 | -0.678869 | 0.095629 | 0.015339 |

| 1979-08-31 | 0.611875 | 1 | 0 | 1.12 | -1.91 | 0.084071 | 0.127019 | 4.694279 | -0.850876 | -0.059612 | -0.678869 | 0.095629 | 0.015339 |

| 1979-09-30 | 0.633431 | 1 | 1 | 1.10 | -2.10 | 0.085207 | 0.073334 | 4.694279 | -0.850876 | -0.059612 | -0.678869 | 0.095629 | 0.015339 |

| 1979-10-31 | 0.754928 | 1 | 0 | 1.27 | -3.47 | 0.075088 | 0.000589 | 4.623207 | -0.850876 | -0.059612 | -0.678869 | 0.095629 | 0.015339 |

| 2019-03-31 | 0.436434 | 1 | 0 | 1.07 | 0.16 | 0.029602 | -0.027690 | 7.949586 | -1.462967 | 0.089407 | -0.667003 | -0.593875 | -0.700222 |

| 2019-04-30 | 0.289830 | 1 | 0 | 1.01 | 0.11 | 0.028409 | 0.082800 | 7.988146 | -1.462967 | 0.089407 | -0.667003 | -0.593875 | -0.700222 |

| 2019-05-31 | 0.421149 | 1 | 0 | 0.96 | 0.01 | 0.028386 | -0.002943 | 7.920105 | -1.462967 | 0.089407 | -0.667003 | -0.593875 | -0.700222 |

| 2019-06-30 | 0.259595 | 1 | 0 | 1.04 | -0.31 | 0.025044 | 0.159981 | 7.986763 | -1.462967 | 0.089407 | -0.667003 | -0.593875 | -0.700222 |

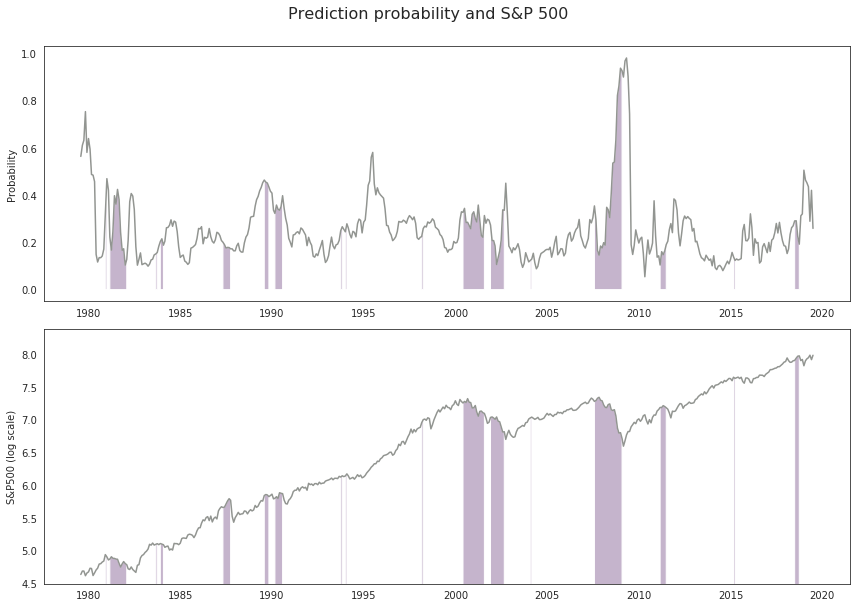

Now to plotting the prediction probability, predictors, intercept and co-efficients.

# Set plot style

sns.set_style('white', {"xtick.major.size": 2, "ytick.major.size": 2})

flatui = ["#c5b4cc", "#3498db", "#95a5a6", "#e74c3c", "#34495e", "#2ecc71","#f4cae4"]

sns.set_palette(sns.color_palette(flatui,7))

# Plot timeseries of SP500, prediction %, and y label shading

fig1, (ax1, ax2) = plt.subplots(nrows = 2)

fig1.suptitle('Prediction probability and S&P 500', size = 16).set_y(1.05)

fig1.subplots_adjust(top = 0.85)

ax1.plot(df_preds_coefs.index, df_preds_coefs['pred_prob'], 'k-',

color = sns.xkcd_rgb['grey'])

ax1.fill_between(

df_preds_coefs.index,

df_preds_coefs['pred_prob'],

y2 = 0,

where = df_preds_coefs['y1']

)

ax1.set_ylabel('Probability')

ax2.plot(df_preds_coefs.index, df_preds_coefs['close'], 'k-',

color = sns.xkcd_rgb['grey'])

ax2.fill_between(

df_preds_coefs.index,

df_preds_coefs['close'],

y2 = 0,

where = df_preds_coefs['y1']

)

ax2.set_ylim(bottom = 4.5)

ax2.set_ylabel('S&P500 (log scale)')

fig1.tight_layout()

Our model is not very good at forecasting the drawdown in the S&P 500. This is not surprising given the little time put into it.

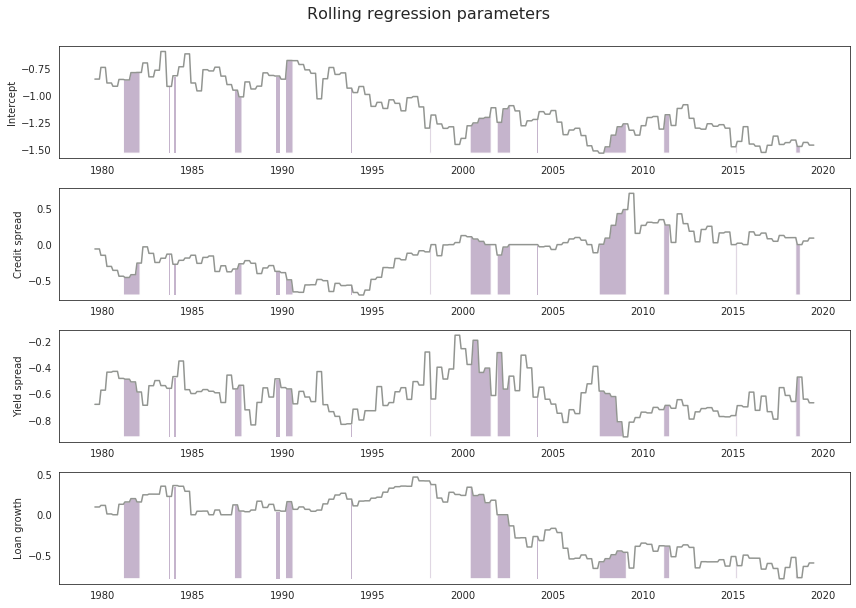

Lets now look at the regression parameters.

# Plot parameters

fig2, (ax1, ax2, ax3, ax4) = plt.subplots(nrows = 4)

fig2.suptitle('Rolling regression parameters', size = 16).set_y(1.05)

fig2.subplots_adjust(top = 0.85)

ax1.plot(df_preds_coefs.index, df_preds_coefs['Int_coef'], 'k-',

color = sns.xkcd_rgb['grey'])

ax1.fill_between(

df_preds_coefs.index,

df_preds_coefs['Int_coef'],

y2 = df_preds_coefs['Int_coef'].min(),

where = df_preds_coefs['y1']

)

ax1.set_ylabel('Intercept')

ax2.plot(df_preds_coefs.index, df_preds_coefs['CRED_SPRD_coef'], 'k-',

color = sns.xkcd_rgb['grey'])

ax2.fill_between(

df_preds_coefs.index,

df_preds_coefs['CRED_SPRD_coef'],

y2 = df_preds_coefs['CRED_SPRD_coef'].min(),

where = df_preds_coefs['y1']

)

ax2.set_ylabel('Credit spread')

ax3.plot(df_preds_coefs.index, df_preds_coefs['YLD_SPRD_coef'], 'k-',

color = sns.xkcd_rgb['grey'])

ax3.fill_between(

df_preds_coefs.index,

df_preds_coefs['YLD_SPRD_coef'],

y2 = df_preds_coefs['YLD_SPRD_coef'].min(),

where = df_preds_coefs['y1']

)

ax3.set_ylabel('Yield spread')

ax4.plot(df_preds_coefs.index, df_preds_coefs['LOAN_GROWTH_coef'], 'k-',

color = sns.xkcd_rgb['grey'])

ax4.fill_between(

df_preds_coefs.index,

df_preds_coefs['LOAN_GROWTH_coef'],

y2 = df_preds_coefs['LOAN_GROWTH_coef'].min(),

where = df_preds_coefs['y1']

)

ax4.set_ylabel('Loan growth')

fig2.tight_layout()

Conclusion

The code embedded in this notebook is working as expected. We have produced a rolling out of sample rolling regression, capturing the prediction probability and regression parameters.

The next steps for this piece of analysis is to embed an inner loop for nested cross validition. This will enable the tuning model hyper-parameters in a time series context.

References

https://towardsdatascience.com/time-series-nested-cross-validation-76adba623eb9

https://github.com/sam31415/timeseriescv/blob/master/timeseriescv/cross_validation.py

https://hub.packtpub.com/cross-validation-strategies-for-time-series-forecasting-tutorial/

https://www.mikulskibartosz.name/nested-cross-validation-in-time-series-forecasting-using-scikit-learn-and-statsmodels/

https://arxiv.org/pdf/1905.11744.pdf